The state of Massachusetts is a no-fault insurance state, meaning most accident victims must pursue insurance claims with their own auto insurance companies after a crash, no matter who was at fault. While this system seems ideal, it restricts when and how a driver can recover compensation for his injuries. In addition, it is not universal for everyone on the road, as motorcycle riders do not receive the same benefits as drivers under this system.

What Is No-Fault Car Insurance?

Everyone on the road in Massachusetts is required to have a minimum auto insurance policy to operate a vehicle. Under our state’s auto insurance laws, these policies must include both liability coverage, which covers other drivers in a collision, and personal injury protection (PIP) for insured driver and his passengers. When two or more cars are in an accident, the drivers and passengers must file claims with their own insurance companies first to cover their bills through their PIP policies. PIP is capped at $8,000 for no-fault coverage, meaning that even if you collided with a tree, you can get your medical bills paid.

If you suffered a serious injury or your medical bills exceed $2,000, you can then file an auto accident claim against the other driver’s insurance company. The other driver is required to have minimum liability coverage, meaning you can receive:

- Up to $20,000 for a single person’s injuries;

- Up to $40,000 for two or more people’s injuries; and

- Up to $5,000 for property damage.

Drivers are also required to have uninsured and underinsured motorist coverage (UM/UIM) that must match their liability insurance minimums. With UM coverage, you can file a claim with your own insurance company if you were injured by an uninsured driver. UIM, in turn, allows you to file a claim with your own insurance company if the other driver does not have enough insurance to cover your costs.

Typically, after a car accident, a driver may first file a claim for PIP coverage and then file a claim against the other driver’s insurance policy. However, for motorcyclists, the process is different.

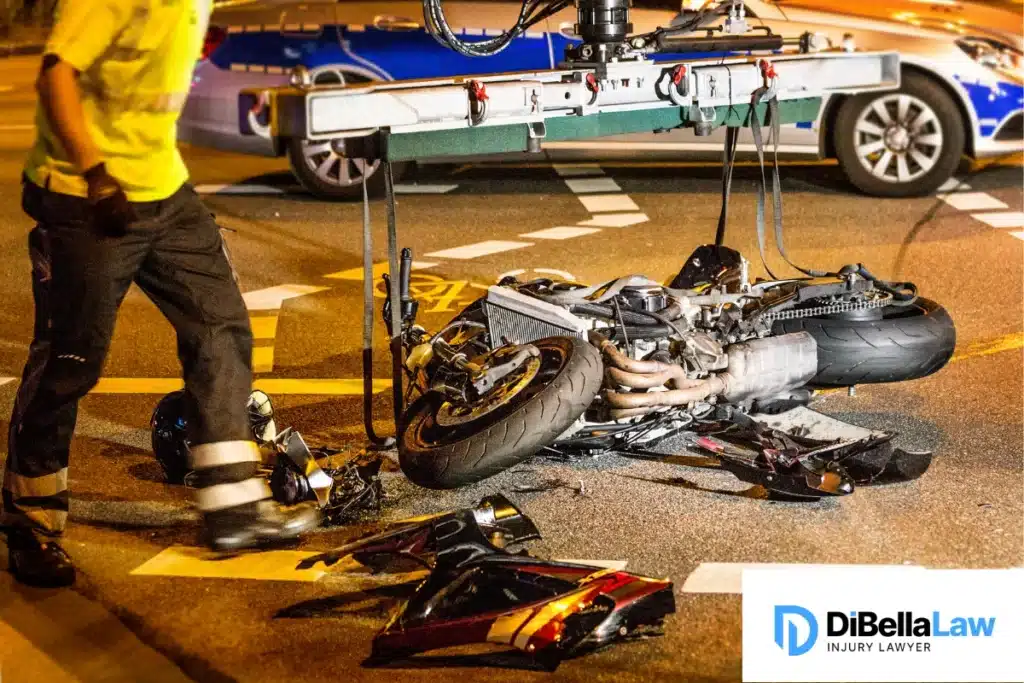

What Options Do Motorcyclists Have?

Motorcyclists are required to have the same minimum liability and UM/UIM policies as other drivers, but auto insurance companies do not have to provide PIP coverage to motorcyclists. Because of this, motorcyclists must file a claim with another driver’s insurance company to recover compensation.

It is important to know that while motorcyclists cannot receive PIP coverage, they can purchase an optional Medical Payment policy (MedPay) that can provide between $5,000 and $10,000. These policies operate in a similar way to PIP and can definitely help a rider get medical treatment after a crash.

Injured in a Motorcycle Accident? Call DiBella Law Injury and Accident Lawyers

Receiving compensation after a motorcycle accident is incredibly difficult. Insurance companies are biased against motorcyclists and not required to offer PIP insurance, so they will fight against paying full compensation for a rider’s injuries. Even if the other driver is 100% at fault, an insurance company may try to pin the blame on you or offer an insultingly low settlement.

Your best option is to talk to a Boston motorcycle accident attorney at DiBella Law Injury and Accident Lawyers We have spent over a decade fighting for motorcyclists who were severely injured by negligent drivers and successfully recovered compensation for their trauma. We know how to deal with dismissive insurance companies and can advocate for your best interests in a settlement negotiation or jury trial. We also work on a contingency-fee basis and offer free consultations, so there is no cost to contacting us at (781) 386-1232.